Written by Rebecca Hampson

March 29, 2019

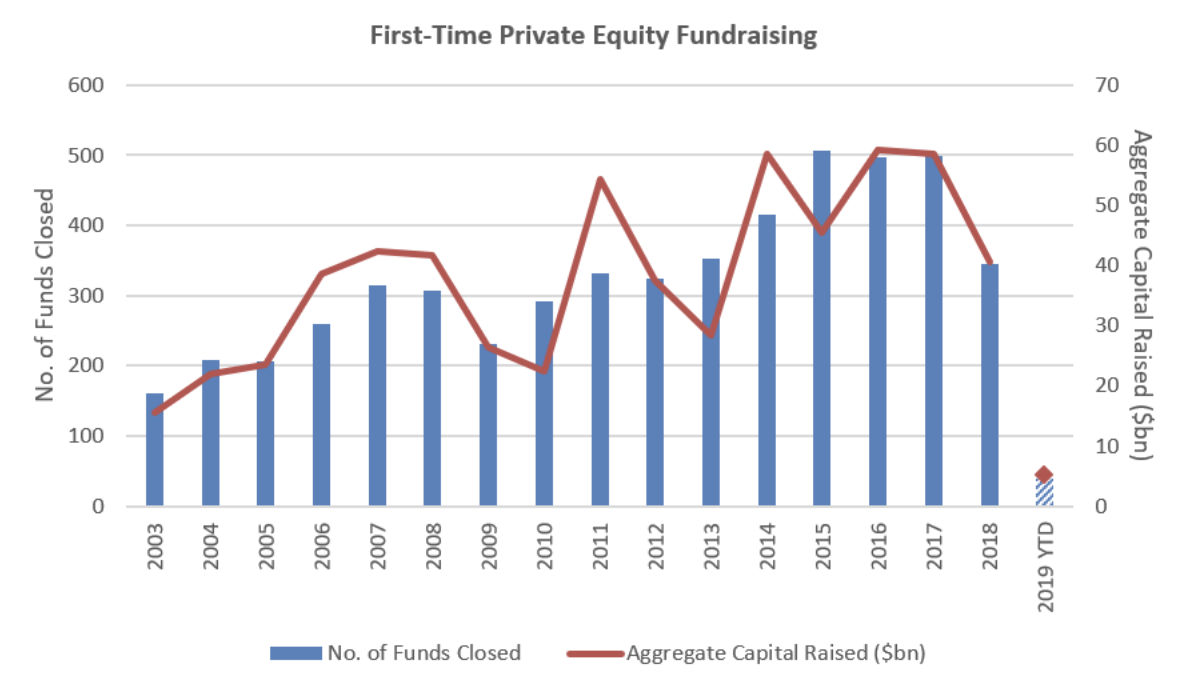

Emerging managers in the private equity and venture capital space have had a difficult year as geopolitical tensions, Brexit and trade wars impact how much capital investors want to put into new and unknown funds. Frustratingly, first-time private equity fundraising dropped to its lowest level last year since 2013. As seen from Preqin in Figure 1 below.

Figure 1: Preqin Data

A combination of uncertainty around geopolitical events, Trump’s trade wars, Brexit and other macro concerns has made markets erratic reducing the number of acquisitions and suppressing valuations and returns. It is prompting investors to take a ‘wait and see’ approach to investing. However, there are a few key things that emerging managers can do to better their chances of a financial commitment.

Here are some guidelines of what those are:

#1 Timing of the Strategy: While a unique strategy, which is verifiable and attributable, is obvious, what is less apparent, but also equally important is the timing of when the strategy is launched.

“Timing of launches is vital for how they position themselves in the market. This is in respect to where and when investors place their cash; investors often allocate 1-2 years in advance.”

~ London-Based Private Equity Lawyer told CreativeCap Advisors

#2 Team’s Deal Experience: It helps if the team has done deals together because it better showcases their ability to source and execute collectively. Investors understand that while timing is key, the real magic lies within the GP skillset and underlying expertise.

“Usually new fund launches are now made off the back of a deal-by-deal strategy executed over a number of months or years – i.e. a fund manager has sourced and funded deals individually and seen verifiable performance on such deals before launching a fund to raise institutional money,” the lawyer further explains.

A seen noted from MJ Hudson: “The teams that do best are those with a history of working together on deals, with overlapping backgrounds and specializations. Most institutional investors regard a firm’s track record and how long its investment team has been together as among the most important factors in their evaluation of GPs competing for commitments. This is among the best evidence that a firm can present to persuade investors that it will safely and profitably put their money to work.”

#3 Fee Structuring: Another considerable value to get their foot into the door with investors and further aid emerging private equity managers is lower economics, although this might mean having to be flexible with their fee structure at an early stage. However, this proves difficult because at the beginning new managers do not have a surplus of cash and they need the income.

James King, Founder and Director of London-based New Model Venture Capital, explains that their fees are variable depending on the product. “As a range, our typical investor will pay between 5-12% upfront and 20%+ as a success fee. Investors in our institutional funds have a typical 2 and 20 model.”

King started his VC firm with £8,750 (US$11,372) nine years ago. It now has just shy of £150m (US$195M) in assets, which is expected to double next year. “At the beginning investors would put in ticket sizes of £30,000 (US$39,000), we now get checks upward of £200,000 (US$260,000),” he says. King attributes his success to various factors, but one includes not being greedy.

King continues to highlight, “our aim is to only manage £100-500m. If you consider that at the low end, we are returning 6x, then that’s 5x profit, I take 20% of that, which is £100m (US$130.7M). Why do I need more than that?” In some of the bigger funds the fund managers live off of the 2% as opposed to the carry, which relies on performance.

As seen in venture capital, the space is facing similar challenges to that of the private equity sector.

King explains: “The biggest challenges we see include emerging managers facing a confirmation bias on the limited partnership side and a huge vested interest in mediocrity. That is, investors who are happy with a 15% return rather than moving shop and getting a 30-40% return.”

As is commonplace in investing there is a certain resistance to change. This is on the basis that it costs money and many investors have a ‘better the devil you know’ mentality. This is the biggest challenge for emerging manager operating in this space because it means they often have to rely on new investors to the market, rather than existing investors with money to invest. Investors also typically go to the better-known VC houses, regardless of track record and performance figures.

“Investor behavior is another issue,” King mentioned. “We find that in the last three years – and particularly in the last nine months – on the back of Brexit – investors are trying to re-negotiate way after a deal has been closed.”

For those starting out he advises that they align their incentives with their investors, but to also show operational capability for the company and for investors.

“What can you actually do for a company on a day-to-day basis and what can you do to enhance the long term returns for investors?,” he asks.

Alongside this, his personal advice to emerging managers is to go and do something else before they start a VC firm. “Learn and get some skills. My business partners and I ran successful companies before we started New Model and it has allowed us to bring different a skillset.”

The biggest challenges we see include emerging managers facing a confirmation bias on the limited partnership side and a huge vested interest in mediocrity. That is, investors who are happy with a 15% return rather than moving shop and getting a 30-40% return.

James King | Founder & Director of New Model Venture Capital

So why should emerging manager venture capital and private equity funds and allocators remain optimistic?

Preqin’s data also shows that there is a good case for emerging managers. As noted from last year, it found that first-time funds delivered higher median net IRRs than established funds in 10-15 vintage years since 2000. Hope remains for these emerging managers, but creating value in numerous different ways as outlined above can help them get to the top of investors’ list.

Are you an emerging fund manager?

We have launched CCA GlobalEssentials™, our new program, offering specialized services to new founders and emerging fund managers.

You have Successfully Subscribed!